" width="150.00000769304802px"><path d="M 0 0 L 9.184 0 L 9.184 1.944 L 0 1.944 Z" fill="rgb(21, 21, 21)" height="1.9444977770054663px" id="gOMgXCMyF" width="9.183673401240327px"/><path d="M 0 0 L 1.913 0 L 1.913 9.334 L 0 9.334 Z M 0 29.945 L 9.184 29.945 L 9.184 31.89 L 0 31.89 Z" fill="rgb(21, 21, 21)" height="31.88976450063828px" id="YKaIqSNTX" width="9.183673401240327px"/><path d="M 0 0 L 1.913 0 L 1.913 9.334 L 0 9.334 Z" fill="rgb(21, 21, 21)" height="9.33358932962625px" id="xNTPXemtb" transform="translate(0 22.556)" width="1.9132652919249722px"/><path d="M 0 0 L 9.184 0 L 9.184 1.944 L 0 1.944 Z" fill="rgb(255, 210, 0)" height="1.9444977770054663px" id="Zg1qA67Pc" transform="translate(140.816 0)" width="9.183673401240355px"/><path d="M 0 0 L 1.913 0 L 1.913 9.334 L 0 9.334 Z" fill="rgb(255, 210, 0)" height="9.333589329626221px" id="F6U7duLaT" transform="translate(148.087 0)" width="1.913265291925029px"/><path d="M 0 0 L 9.184 0 L 9.184 1.944 L 0 1.944 Z" fill="rgb(21, 21, 21)" height="1.9444977770054663px" id="vS19iM8bf" transform="translate(140.816 29.945)" width="9.183673401240355px"/><path d="M 135.077 14.558 L 136.99 14.558 L 136.99 23.891 L 135.077 23.891 Z M 4.898 11.072 C 5.528 11.072 6.009 10.838 6.34 10.371 C 6.673 9.902 6.84 9.222 6.84 8.331 C 6.84 7.44 6.673 6.761 6.34 6.294 C 6.009 5.825 5.528 5.59 4.898 5.59 C 4.269 5.59 3.785 5.826 3.446 6.297 C 3.109 6.767 2.941 7.445 2.941 8.331 C 2.941 9.217 3.109 9.895 3.446 10.366 C 3.785 10.836 4.269 11.072 4.898 11.072 Z M 2.941 5.013 C 3.348 4.468 3.798 4.066 4.291 3.807 C 4.784 3.549 5.351 3.42 5.993 3.42 C 7.127 3.42 8.059 3.878 8.786 4.794 C 9.516 5.71 9.881 6.889 9.881 8.331 C 9.881 9.773 9.516 10.953 8.786 11.871 C 8.059 12.787 7.127 13.246 5.993 13.246 C 5.351 13.246 4.784 13.116 4.291 12.858 C 3.798 12.597 3.348 12.195 2.941 11.649 L 2.941 13.002 L 0 13.002 L 0 0 L 2.941 0 Z M 18.892 6.192 C 18.634 6.069 18.377 5.979 18.121 5.922 C 17.867 5.863 17.611 5.834 17.353 5.834 C 16.597 5.834 16.015 6.081 15.606 6.575 C 15.197 7.067 14.993 7.772 14.993 8.69 L 14.993 13.002 L 12.052 13.002 L 12.052 3.644 L 14.993 3.644 L 14.993 5.182 C 15.372 4.569 15.806 4.122 16.295 3.842 C 16.786 3.56 17.375 3.42 18.06 3.42 C 18.159 3.42 18.265 3.424 18.379 3.433 C 18.495 3.44 18.662 3.458 18.881 3.486 Z M 29.544 8.299 L 29.544 9.149 L 22.665 9.149 C 22.735 9.852 22.984 10.378 23.412 10.729 C 23.84 11.081 24.437 11.256 25.204 11.256 C 25.823 11.256 26.457 11.163 27.106 10.976 C 27.756 10.788 28.425 10.506 29.11 10.128 L 29.11 12.433 C 28.414 12.7 27.718 12.902 27.021 13.039 C 26.325 13.177 25.629 13.246 24.933 13.246 C 23.267 13.246 21.971 12.815 21.047 11.954 C 20.125 11.093 19.663 9.885 19.663 8.331 C 19.663 6.805 20.117 5.606 21.023 4.733 C 21.93 3.857 23.179 3.42 24.77 3.42 C 26.216 3.42 27.374 3.863 28.242 4.748 C 29.11 5.633 29.544 6.816 29.544 8.299 Z M 26.519 7.304 C 26.519 6.736 26.356 6.278 26.03 5.93 C 25.704 5.581 25.277 5.406 24.751 5.406 C 24.181 5.406 23.718 5.569 23.362 5.895 C 23.006 6.221 22.784 6.691 22.697 7.304 Z M 35.899 8.791 C 35.286 8.791 34.823 8.897 34.513 9.109 C 34.204 9.319 34.05 9.631 34.05 10.045 C 34.05 10.423 34.174 10.72 34.423 10.935 C 34.674 11.149 35.021 11.256 35.465 11.256 C 36.018 11.256 36.483 11.055 36.862 10.652 C 37.241 10.247 37.43 9.741 37.43 9.133 L 37.43 8.791 Z M 40.398 7.663 L 40.398 13.002 L 37.43 13.002 L 37.43 11.614 C 37.036 12.183 36.591 12.597 36.096 12.858 C 35.604 13.116 35.004 13.246 34.297 13.246 C 33.343 13.246 32.569 12.963 31.974 12.398 C 31.38 11.831 31.083 11.097 31.083 10.195 C 31.083 9.097 31.453 8.292 32.195 7.78 C 32.939 7.267 34.105 7.01 35.694 7.01 L 37.43 7.01 L 37.43 6.778 C 37.43 6.304 37.246 5.957 36.878 5.738 C 36.511 5.517 35.939 5.406 35.16 5.406 C 34.53 5.406 33.944 5.47 33.4 5.599 C 32.858 5.727 32.354 5.919 31.887 6.176 L 31.887 3.896 C 32.519 3.739 33.152 3.62 33.787 3.54 C 34.423 3.46 35.059 3.42 35.694 3.42 C 37.355 3.42 38.554 3.752 39.29 4.417 C 40.029 5.082 40.398 6.164 40.398 7.663 Z M 43.136 0 L 46.077 0 L 46.077 7.077 L 49.466 3.644 L 52.885 3.644 L 48.387 7.938 L 53.238 13.002 L 49.671 13.002 L 46.077 9.101 L 46.077 13.002 L 43.136 13.002 Z" fill="rgb(21, 21, 21)" height="23.89126564493384px" id="BgbathAjS" transform="translate(13.01 7.972)" width="136.98980327397163px"/><path d="M 4.423 0 L 6.29 0 L 1.859 14.383 L 0 14.383 Z" fill="rgb(255, 210, 0)" height="14.383450056509389px" id="CwSlx98Zu" transform="translate(76.148 8.556)" width="6.290433626791241px"/><path d="M 6.921 11.414 C 6.516 11.959 6.069 12.36 5.58 12.617 C 5.092 12.874 4.528 13.002 3.888 13.002 C 2.764 13.002 1.834 12.553 1.1 11.655 C 0.367 10.754 0 9.607 0 8.214 C 0 6.816 0.367 5.671 1.1 4.778 C 1.834 3.883 2.764 3.436 3.888 3.436 C 4.528 3.436 5.092 3.564 5.58 3.821 C 6.069 4.075 6.516 4.479 6.921 5.032 L 6.921 3.644 L 9.881 3.644 L 9.881 12.058 C 9.881 13.563 9.414 14.712 8.479 15.505 C 7.544 16.298 6.189 16.694 4.414 16.694 C 3.839 16.694 3.282 16.65 2.744 16.561 C 2.207 16.472 1.668 16.335 1.126 16.152 L 1.126 13.82 C 1.64 14.122 2.143 14.346 2.636 14.494 C 3.13 14.642 3.627 14.716 4.125 14.716 C 5.09 14.716 5.796 14.501 6.245 14.072 C 6.696 13.642 6.921 12.971 6.921 12.058 Z M 4.98 5.59 C 4.371 5.59 3.897 5.819 3.557 6.278 C 3.218 6.734 3.049 7.379 3.049 8.214 C 3.049 9.073 3.213 9.723 3.541 10.165 C 3.871 10.607 4.35 10.829 4.98 10.829 C 5.594 10.829 6.071 10.6 6.411 10.144 C 6.751 9.688 6.921 9.044 6.921 8.214 C 6.921 7.379 6.751 6.734 6.411 6.278 C 6.071 5.819 5.594 5.59 4.98 5.59 Z M 12.71 0 L 15.651 0 L 15.651 13.002 L 12.71 13.002 Z M 22.606 8.791 C 21.992 8.791 21.53 8.897 21.22 9.109 C 20.911 9.319 20.757 9.631 20.757 10.045 C 20.757 10.423 20.881 10.72 21.13 10.935 C 21.381 11.149 21.728 11.256 22.172 11.256 C 22.724 11.256 23.19 11.055 23.569 10.652 C 23.948 10.247 24.137 9.741 24.137 9.133 L 24.137 8.791 Z M 27.104 7.663 L 27.104 13.002 L 24.137 13.002 L 24.137 11.614 C 23.742 12.183 23.298 12.597 22.803 12.858 C 22.31 13.116 21.711 13.246 21.004 13.246 C 20.05 13.246 19.275 12.963 18.681 12.398 C 18.086 11.831 17.789 11.097 17.789 10.195 C 17.789 9.097 18.16 8.292 18.902 7.78 C 19.646 7.267 20.812 7.01 22.401 7.01 L 24.137 7.01 L 24.137 6.778 C 24.137 6.304 23.953 5.957 23.584 5.738 C 23.218 5.517 22.646 5.406 21.867 5.406 C 21.237 5.406 20.651 5.47 20.107 5.599 C 19.565 5.727 19.06 5.919 18.594 6.176 L 18.594 3.896 C 19.225 3.739 19.858 3.62 20.493 3.54 C 21.13 3.46 21.766 3.42 22.401 3.42 C 24.062 3.42 25.26 3.752 25.997 4.417 C 26.735 5.082 27.104 6.164 27.104 7.663 Z M 37.035 3.936 L 37.035 6.208 C 36.405 5.941 35.797 5.74 35.209 5.607 C 34.623 5.473 34.07 5.406 33.549 5.406 C 32.99 5.406 32.574 5.477 32.302 5.62 C 32.032 5.763 31.897 5.981 31.897 6.275 C 31.897 6.516 32 6.7 32.205 6.829 C 32.41 6.955 32.778 7.05 33.31 7.112 L 33.828 7.187 C 35.336 7.381 36.35 7.701 36.869 8.147 C 37.39 8.592 37.65 9.292 37.65 10.246 C 37.65 11.242 37.288 11.991 36.564 12.494 C 35.841 12.995 34.763 13.246 33.328 13.246 C 32.72 13.246 32.09 13.196 31.439 13.098 C 30.79 13 30.123 12.854 29.438 12.66 L 29.438 10.387 C 30.025 10.676 30.627 10.893 31.242 11.04 C 31.859 11.184 32.486 11.256 33.121 11.256 C 33.697 11.256 34.13 11.176 34.42 11.016 C 34.711 10.853 34.857 10.613 34.857 10.294 C 34.857 10.026 34.757 9.827 34.557 9.697 C 34.357 9.567 33.958 9.466 33.36 9.393 L 32.842 9.326 C 31.531 9.158 30.613 8.849 30.087 8.398 C 29.561 7.947 29.298 7.262 29.298 6.342 C 29.298 5.351 29.632 4.616 30.3 4.139 C 30.97 3.659 31.995 3.42 33.375 3.42 C 33.919 3.42 34.489 3.461 35.085 3.545 C 35.684 3.627 36.334 3.757 37.035 3.936 Z M 47.056 3.936 L 47.056 6.208 C 46.427 5.941 45.818 5.74 45.231 5.607 C 44.645 5.473 44.091 5.406 43.571 5.406 C 43.011 5.406 42.595 5.477 42.324 5.62 C 42.054 5.763 41.918 5.981 41.918 6.275 C 41.918 6.516 42.021 6.7 42.226 6.829 C 42.432 6.955 42.8 7.05 43.331 7.112 L 43.849 7.187 C 45.358 7.381 46.372 7.701 46.891 8.147 C 47.412 8.592 47.672 9.292 47.672 10.246 C 47.672 11.242 47.31 11.991 46.585 12.494 C 45.863 12.995 44.784 13.246 43.35 13.246 C 42.741 13.246 42.111 13.196 41.461 13.098 C 40.812 13 40.145 12.854 39.459 12.66 L 39.459 10.387 C 40.046 10.676 40.648 10.893 41.263 11.04 C 41.881 11.184 42.507 11.256 43.142 11.256 C 43.719 11.256 44.152 11.176 44.441 11.016 C 44.732 10.853 44.878 10.613 44.878 10.294 C 44.878 10.026 44.778 9.827 44.578 9.697 C 44.378 9.567 43.979 9.466 43.381 9.393 L 42.863 9.326 C 41.553 9.158 40.635 8.849 40.109 8.398 C 39.583 7.947 39.32 7.262 39.32 6.342 C 39.32 5.351 39.654 4.616 40.322 4.139 C 40.992 3.659 42.017 3.42 43.397 3.42 C 43.941 3.42 44.511 3.461 45.107 3.545 C 45.705 3.627 46.355 3.757 47.056 3.936 Z" fill="rgb(21, 21, 21)" height="16.694290834220567px" id="dLc4QLWwi" transform="translate(93.176 7.972)" width="47.67206679668203px"/></g></svg>)

Table of contents

Share on Social Media

The ROI of research-driven thought leadership

The Harris Poll's 2022 thought leadership study surveyed 500 US executives at the director level and above. Two of the numbers in that study, taken together, produce a claim that should make any honest marketer uncomfortable. Companies spend an average of $194,000 per year on thought leadership. Executives estimate the total annual value of that thought leadership at $2.7 million. The return is roughly 14 to 1.

That number doesn't appear anywhere else in a B2B marketing budget. Paid search returns sit at 2 to 4x. Trade show ROI lands between 5 and 10x and usually requires generous assumptions to get there. A 14x return on anything in B2B should be treated as wrong until proven otherwise.

So either the Harris number is wrong, or thought leadership is doing something most marketing line items can't do. The honest answer is that the number is right but only for one specific thing, which is real research-driven thought leadership rather than the content marketing most firms confuse it with.

The rest of this post traces where the 14x actually comes from, across six places in and around the sales funnel, with hypothetical math you can adjust to your own firm. But here's a 10k ft. view.

The hypothetical firm we'll use throughout

To keep the math grounded, the rest of this post uses a single model firm. A $30 million mid-market consulting firm. Average deal size of $400,000. Forty RFP responses per year. Current shortlist rate of 30%, which produces twelve finalist appearances. Current win rate from shortlist of 25%, which produces three RFP wins per year and about $1.2 million of RFP revenue. The existing client book is approximately $15 million of recurring or expandable accounts. The remainder of the firm's revenue comes from referrals, retained client work, and one-off engagements outside the RFP pipeline.

Those numbers are made up. They're meant to be plausible for a real mid-market firm, but the point is that the math scales linearly. Substitute your firm's actual figures and the conclusions hold. I'll also show what each ROI category looks like at different deal sizes, since the dollar amounts move materially depending on whether your average engagement is $250K or $750K.

1. More invitations to bid

Buyers who read your research start the buying process with your firm already in mind. Some of them become unsolicited inquiries. Others become RFPs you wouldn't have been invited to. A few become introductions through partners or former colleagues who remembered something you published.

Inbound deals close at a higher rate than cold RFPs because the buyer chose you, not the other way around. The first call is shorter because the explanation work is mostly done. The reference check is lighter because the research is itself a kind of reference.

The math. Assume three incremental inbound opportunities per year that wouldn't have come to the firm otherwise. At a 50% close rate (a reasonable assumption for warm inbound), the firm wins about 1.5 of them. At the model firm's $400K deal size: $600K of new revenue. At a smaller boutique with $250K deals: $375K. At a larger firm with $750K deals: $1.125M. None of these are large enough on their own to justify a research program, which is the point. The case has to be made across categories.

2. Higher shortlist rates

Buyers running an RFP typically narrow eight to twelve firms to three or four finalists. The shortlist decision is heavily influenced by who looks credible at the credentials stage, which is the earliest and most pattern-matching stage of the process. Most buyers are sifting fast, and the firms that look serious make the cut.

A firm with cited research has a structural advantage at that stage. Generic capabilities decks blur together. Original research doesn't. The credentials reviewer is looking for reasons to advance some firms and cut others, and "they published a study on this exact topic last quarter" is a clean reason.

The math. The model firm runs 40 RFPs per year with a current shortlist rate of 30%. If the shortlist rate moves to 40%, that's four additional shortlist appearances per year. At the firm's current 25% win rate and $400K deal size: one more RFP win, or $400K of additional revenue. At $750K deals: $750K. For a larger firm running 80 RFPs annually with the same ten-point improvement, the math doubles to $800K at $400K deals.

3. Higher win rates from the shortlist

At the finalist stage, the buyer has decided your firm is capable. The question is no longer whether you can do the work. It's whether you're the right partner for this particular work. The decision factors are fit, trust, and perceived risk.

Research-driven thought leadership moves all three. The research itself shows the firm has thought about the buyer's problem before the buyer brought it to them, which signals fit. Cited work lowers perceived risk by giving the internal champion something concrete to point at when arguing for the firm. And when both finalists are credible on paper, the firm whose research the procurement team actually read tends to win the room.

The math. Of the model firm's twelve baseline shortlist appearances at a 25% win rate, the firm wins three RFPs and produces $1.2M of revenue. If win rate moves to 30%, the firm wins 3.6 RFPs. A five-point win rate improvement at $400K deals is roughly $240K per year. At $750K deals, the same five-point move is roughly $450K. Combine this with the shortlist improvement from the previous section and the firm's RFP outcomes step from three wins to roughly 4.8, from $1.2M to $1.92M of RFP revenue. A net incremental gain of about $720K from the two effects combined.

4. Shorter sales cycles

Every sales cycle has friction at each stage. Explaining what your firm does. Justifying the approach. Getting reference calls scheduled. Navigating internal hesitation about hiring an unfamiliar firm. Research-driven thought leadership doesn't eliminate any of those stages, but it collapses several of them because the buyer arrives at the first meeting already familiar with the firm's point of view.

Cycle time is the actual constraint on a senior seller's pipeline. Most partners aren't lead-starved. They're capacity-starved. A six-month cycle that becomes a four-and-a-half month cycle frees up real selling time, which converts to additional deals through the same pipeline.

The math. A partner running eight deals per year at a six-month average cycle becomes a partner running ten to eleven deals per year at a 4.5-month cycle. At a 25% win rate and $400K deals, that's a baseline of roughly $800K of revenue becoming roughly $1.07M. The difference is $250K to $300K per partner per year. A firm with three senior sellers and a similar cycle improvement: $750K to $900K in additional revenue from the cycle effect alone.

5. Account expansion

Existing clients who read your research on adjacent practice areas start asking about those services. A strategy firm that publishes original research on operational performance gets pulled into operations conversations. A firm doing CFO-level advisory work that publishes on talent operations gets asked about talent operations. The research signals capability in the adjacent area without requiring a new sales motion.

This is the most underrated ROI category because the dollars are large and the mechanism is invisible. Nobody attributes account expansion to a research publication. Clients themselves usually attribute it to "we needed help with X anyway and we already know you." But the research is what made them connect "we already know you" to "you can help us with this new problem."

The math. The model firm has $15M of expandable client book. At 5% incremental year-over-year expansion attributable to the research surfacing adjacent capabilities, that's $750K per year. At 10%, it's $1.5M. Critically, this recurs annually. Over a three-year client relationship at the 5% figure, the math produces $2.25M of additional revenue from a single year's research program continuing to surface adjacent work.

6. Talent attraction and retention

Senior consulting hires made through a recruiter cost $50K to $150K in fees, depending on the role and the firm. That's before counting partner time spent interviewing, the cost of bad hires that don't work out, and the gap revenue while the seat is empty. A realistic fully-loaded cost of a senior recruiter hire is $200K to $400K.

Senior departures are worse. Replacement plus disruption costs at the senior level run $300K to $500K, and that's before accounting for the relationships and institutional knowledge that walk out the door with them.

Firms with strong intellectual reputations attract inbound applications, which shifts some senior hiring away from recruiters. They also retain senior people longer. Senior consultants stay where the work feels intellectually serious, and a research program is one of the clearest signals that the work is intellectually serious.

The math. Shift one senior hire per year from recruiter to inbound: $75K to $150K saved in fees alone, $200K to $400K saved counting partner time and gap revenue. Retain one senior person who would otherwise have left: $300K to $500K avoided. Combined annual impact for a firm where these effects add up across the partner group: $500K to $900K of cost avoidance per year.

Running the whole model

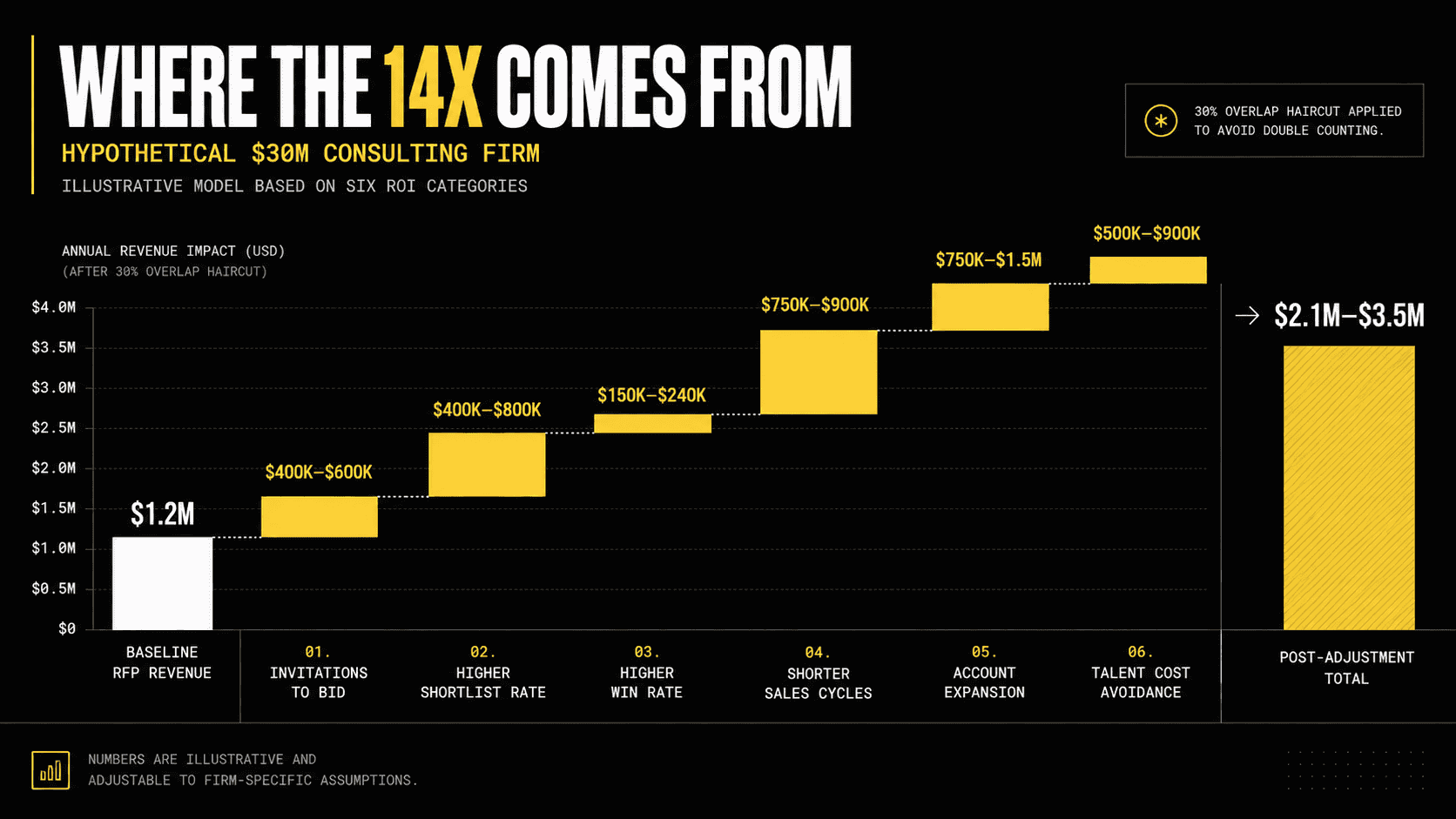

Stacking the six categories produces a consolidated annual ROI estimate for the hypothetical $30M firm at $400K average deals. Each line uses the conservative-to-aggressive range described in its section.

Category | Annual impact (low) | Annual impact (high) |

|---|---|---|

More invitations to bid | $400K | $600K |

Higher shortlist rate | $400K | $800K |

Higher win rate | $150K | $240K |

Shorter sales cycles (3 sellers) | $750K | $900K |

Account expansion (year 1) | $750K | $1.5M |

Talent cost avoidance | $500K | $900K |

Total before adjustment | $2.95M | $4.94M |

Two of these categories overlap. The shortlist and win rate improvements share an underlying mechanism with the cycle time gains, since brand authority operates at multiple stages of the same sales process. An honest model haircuts the overlap by roughly 30%.

After that adjustment, annual impact lands between $2.1M and $3.5M.

Against an investment of $100K to $200K for a serious research-driven program, that's a return of roughly 10x to 25x.

Harris's 14x figure sits roughly in the middle of that range. Which is what you'd expect from a survey average that includes firms running generic content programs alongside firms running real research-anchored work. The average pulls both into a single number that disguises the gap between them. Firms running real research-driven thought leadership land in the upper half of the range. Firms running content marketing land closer to zero, and they pull the average down.

This is where the real-versus-content distinction stops being a framing device and becomes the load-bearing claim. The math above only works if the research is real enough to generate the effects. Generic content doesn't move shortlist rates because it isn't differentiated enough to do so. Generic content doesn't shorten sales cycles because the buyer has nothing distinctive to remember. Generic content doesn't retain a senior consultant because there's nothing intellectually serious for them to be part of.

The 14x figure is the average of two very different things. The bet on research-driven thought leadership is the bet that your firm lands in the half of the distribution earning meaningful returns instead of the half that isn't.

How to actually measure this in your firm

Three things to start tracking, none of which require new software.

Tag every inbound inquiry with how the prospect found the firm. Most CRMs already have a field for source. Use it consistently. After six months you'll have a defensible signal on whether published research is generating inbound, and whether that inbound closes at a higher rate than other sources.

Ask every new client during onboarding what they read or saw from the firm before reaching out. Two questions: "What was the first piece of our work you came across?" and "What made you decide to call us?" Most clients answer honestly because they're not yet in negotiation mode.

Keep a simple log of shortlist invitations against the publication calendar. If the firm published a major piece of research in March, look at the shortlist rate from April through September and compare it to the prior twelve months. Six months of data is enough to see whether the ratio moved.

None of this is sophisticated attribution modeling. It's a closer approximation of reality than what most firms have. If the effects are real for your firm, the math becomes obvious in your own numbers within a year. If they're not, the diagnosis usually isn't that thought leadership doesn't work. It's that the research isn't real enough to be worth measuring.

The ROI of research-driven thought leadership

The Harris Poll's 2022 thought leadership study surveyed 500 US executives at the director level and above. Two of the numbers in that study, taken together, produce a claim that should make any honest marketer uncomfortable. Companies spend an average of $194,000 per year on thought leadership. Executives estimate the total annual value of that thought leadership at $2.7 million. The return is roughly 14 to 1.

That number doesn't appear anywhere else in a B2B marketing budget. Paid search returns sit at 2 to 4x. Trade show ROI lands between 5 and 10x and usually requires generous assumptions to get there. A 14x return on anything in B2B should be treated as wrong until proven otherwise.

So either the Harris number is wrong, or thought leadership is doing something most marketing line items can't do. The honest answer is that the number is right but only for one specific thing, which is real research-driven thought leadership rather than the content marketing most firms confuse it with.

The rest of this post traces where the 14x actually comes from, across six places in and around the sales funnel, with hypothetical math you can adjust to your own firm. But here's a 10k ft. view.

The hypothetical firm we'll use throughout

To keep the math grounded, the rest of this post uses a single model firm. A $30 million mid-market consulting firm. Average deal size of $400,000. Forty RFP responses per year. Current shortlist rate of 30%, which produces twelve finalist appearances. Current win rate from shortlist of 25%, which produces three RFP wins per year and about $1.2 million of RFP revenue. The existing client book is approximately $15 million of recurring or expandable accounts. The remainder of the firm's revenue comes from referrals, retained client work, and one-off engagements outside the RFP pipeline.

Those numbers are made up. They're meant to be plausible for a real mid-market firm, but the point is that the math scales linearly. Substitute your firm's actual figures and the conclusions hold. I'll also show what each ROI category looks like at different deal sizes, since the dollar amounts move materially depending on whether your average engagement is $250K or $750K.

1. More invitations to bid

Buyers who read your research start the buying process with your firm already in mind. Some of them become unsolicited inquiries. Others become RFPs you wouldn't have been invited to. A few become introductions through partners or former colleagues who remembered something you published.

Inbound deals close at a higher rate than cold RFPs because the buyer chose you, not the other way around. The first call is shorter because the explanation work is mostly done. The reference check is lighter because the research is itself a kind of reference.

The math. Assume three incremental inbound opportunities per year that wouldn't have come to the firm otherwise. At a 50% close rate (a reasonable assumption for warm inbound), the firm wins about 1.5 of them. At the model firm's $400K deal size: $600K of new revenue. At a smaller boutique with $250K deals: $375K. At a larger firm with $750K deals: $1.125M. None of these are large enough on their own to justify a research program, which is the point. The case has to be made across categories.

2. Higher shortlist rates

Buyers running an RFP typically narrow eight to twelve firms to three or four finalists. The shortlist decision is heavily influenced by who looks credible at the credentials stage, which is the earliest and most pattern-matching stage of the process. Most buyers are sifting fast, and the firms that look serious make the cut.

A firm with cited research has a structural advantage at that stage. Generic capabilities decks blur together. Original research doesn't. The credentials reviewer is looking for reasons to advance some firms and cut others, and "they published a study on this exact topic last quarter" is a clean reason.

The math. The model firm runs 40 RFPs per year with a current shortlist rate of 30%. If the shortlist rate moves to 40%, that's four additional shortlist appearances per year. At the firm's current 25% win rate and $400K deal size: one more RFP win, or $400K of additional revenue. At $750K deals: $750K. For a larger firm running 80 RFPs annually with the same ten-point improvement, the math doubles to $800K at $400K deals.

3. Higher win rates from the shortlist

At the finalist stage, the buyer has decided your firm is capable. The question is no longer whether you can do the work. It's whether you're the right partner for this particular work. The decision factors are fit, trust, and perceived risk.

Research-driven thought leadership moves all three. The research itself shows the firm has thought about the buyer's problem before the buyer brought it to them, which signals fit. Cited work lowers perceived risk by giving the internal champion something concrete to point at when arguing for the firm. And when both finalists are credible on paper, the firm whose research the procurement team actually read tends to win the room.

The math. Of the model firm's twelve baseline shortlist appearances at a 25% win rate, the firm wins three RFPs and produces $1.2M of revenue. If win rate moves to 30%, the firm wins 3.6 RFPs. A five-point win rate improvement at $400K deals is roughly $240K per year. At $750K deals, the same five-point move is roughly $450K. Combine this with the shortlist improvement from the previous section and the firm's RFP outcomes step from three wins to roughly 4.8, from $1.2M to $1.92M of RFP revenue. A net incremental gain of about $720K from the two effects combined.

4. Shorter sales cycles

Every sales cycle has friction at each stage. Explaining what your firm does. Justifying the approach. Getting reference calls scheduled. Navigating internal hesitation about hiring an unfamiliar firm. Research-driven thought leadership doesn't eliminate any of those stages, but it collapses several of them because the buyer arrives at the first meeting already familiar with the firm's point of view.

Cycle time is the actual constraint on a senior seller's pipeline. Most partners aren't lead-starved. They're capacity-starved. A six-month cycle that becomes a four-and-a-half month cycle frees up real selling time, which converts to additional deals through the same pipeline.

The math. A partner running eight deals per year at a six-month average cycle becomes a partner running ten to eleven deals per year at a 4.5-month cycle. At a 25% win rate and $400K deals, that's a baseline of roughly $800K of revenue becoming roughly $1.07M. The difference is $250K to $300K per partner per year. A firm with three senior sellers and a similar cycle improvement: $750K to $900K in additional revenue from the cycle effect alone.

5. Account expansion

Existing clients who read your research on adjacent practice areas start asking about those services. A strategy firm that publishes original research on operational performance gets pulled into operations conversations. A firm doing CFO-level advisory work that publishes on talent operations gets asked about talent operations. The research signals capability in the adjacent area without requiring a new sales motion.

This is the most underrated ROI category because the dollars are large and the mechanism is invisible. Nobody attributes account expansion to a research publication. Clients themselves usually attribute it to "we needed help with X anyway and we already know you." But the research is what made them connect "we already know you" to "you can help us with this new problem."

The math. The model firm has $15M of expandable client book. At 5% incremental year-over-year expansion attributable to the research surfacing adjacent capabilities, that's $750K per year. At 10%, it's $1.5M. Critically, this recurs annually. Over a three-year client relationship at the 5% figure, the math produces $2.25M of additional revenue from a single year's research program continuing to surface adjacent work.

6. Talent attraction and retention

Senior consulting hires made through a recruiter cost $50K to $150K in fees, depending on the role and the firm. That's before counting partner time spent interviewing, the cost of bad hires that don't work out, and the gap revenue while the seat is empty. A realistic fully-loaded cost of a senior recruiter hire is $200K to $400K.

Senior departures are worse. Replacement plus disruption costs at the senior level run $300K to $500K, and that's before accounting for the relationships and institutional knowledge that walk out the door with them.

Firms with strong intellectual reputations attract inbound applications, which shifts some senior hiring away from recruiters. They also retain senior people longer. Senior consultants stay where the work feels intellectually serious, and a research program is one of the clearest signals that the work is intellectually serious.

The math. Shift one senior hire per year from recruiter to inbound: $75K to $150K saved in fees alone, $200K to $400K saved counting partner time and gap revenue. Retain one senior person who would otherwise have left: $300K to $500K avoided. Combined annual impact for a firm where these effects add up across the partner group: $500K to $900K of cost avoidance per year.

Running the whole model

Stacking the six categories produces a consolidated annual ROI estimate for the hypothetical $30M firm at $400K average deals. Each line uses the conservative-to-aggressive range described in its section.

Category | Annual impact (low) | Annual impact (high) |

|---|---|---|

More invitations to bid | $400K | $600K |

Higher shortlist rate | $400K | $800K |

Higher win rate | $150K | $240K |

Shorter sales cycles (3 sellers) | $750K | $900K |

Account expansion (year 1) | $750K | $1.5M |

Talent cost avoidance | $500K | $900K |

Total before adjustment | $2.95M | $4.94M |

Two of these categories overlap. The shortlist and win rate improvements share an underlying mechanism with the cycle time gains, since brand authority operates at multiple stages of the same sales process. An honest model haircuts the overlap by roughly 30%.

After that adjustment, annual impact lands between $2.1M and $3.5M.

Against an investment of $100K to $200K for a serious research-driven program, that's a return of roughly 10x to 25x.

Harris's 14x figure sits roughly in the middle of that range. Which is what you'd expect from a survey average that includes firms running generic content programs alongside firms running real research-anchored work. The average pulls both into a single number that disguises the gap between them. Firms running real research-driven thought leadership land in the upper half of the range. Firms running content marketing land closer to zero, and they pull the average down.

This is where the real-versus-content distinction stops being a framing device and becomes the load-bearing claim. The math above only works if the research is real enough to generate the effects. Generic content doesn't move shortlist rates because it isn't differentiated enough to do so. Generic content doesn't shorten sales cycles because the buyer has nothing distinctive to remember. Generic content doesn't retain a senior consultant because there's nothing intellectually serious for them to be part of.

The 14x figure is the average of two very different things. The bet on research-driven thought leadership is the bet that your firm lands in the half of the distribution earning meaningful returns instead of the half that isn't.

How to actually measure this in your firm

Three things to start tracking, none of which require new software.

Tag every inbound inquiry with how the prospect found the firm. Most CRMs already have a field for source. Use it consistently. After six months you'll have a defensible signal on whether published research is generating inbound, and whether that inbound closes at a higher rate than other sources.

Ask every new client during onboarding what they read or saw from the firm before reaching out. Two questions: "What was the first piece of our work you came across?" and "What made you decide to call us?" Most clients answer honestly because they're not yet in negotiation mode.

Keep a simple log of shortlist invitations against the publication calendar. If the firm published a major piece of research in March, look at the shortlist rate from April through September and compare it to the prior twelve months. Six months of data is enough to see whether the ratio moved.

None of this is sophisticated attribution modeling. It's a closer approximation of reality than what most firms have. If the effects are real for your firm, the math becomes obvious in your own numbers within a year. If they're not, the diagnosis usually isn't that thought leadership doesn't work. It's that the research isn't real enough to be worth measuring.